Board

Pre-read.

June 2026

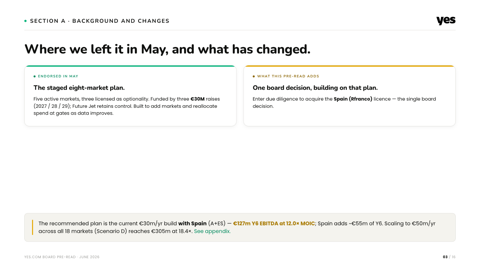

Where we left it in May, and what has changed.

The staged eight-market plan.

Five active markets, three licensed as optionality. Funded by three €30M raises (2027 / 28 / 29); Future Jet retains control. Built to add markets and reallocate spend at gates as data improves.

One board decision, building on that plan.

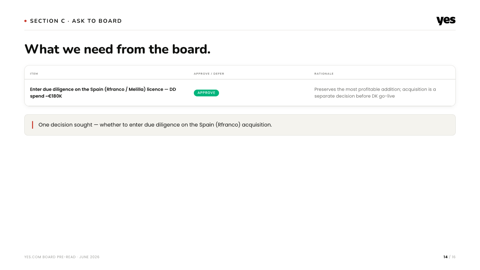

Enter due diligence to acquire the Spain (Rfranco) licence — the single board decision.

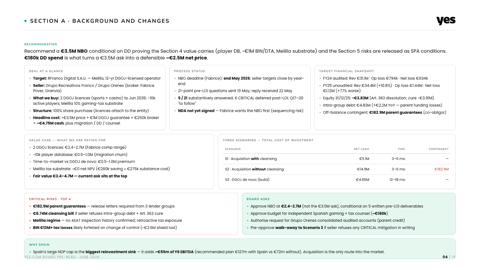

Recommend a €3.5M NBO conditional on DD proving the Section 4 value carries (player DB, ~€1M BIN/DTA, Melilla substrate) and the Section 5 risks are released as SPA conditions. €180k DD spend is what turns a €3.5M ask into a defensible ~€2.5M net price.

- Target: RFranco Digital S.A.U. — Melilla, 12-yr DGOJ-licensed operator

- Seller: Grupo Recreativos Franco / Grupo Orenes (broker: Fabrice Pover, Granvia)

- What we buy: 2 DGOJ licences (sports + casino) to Jun 2035; ~10k active players; Melilla 10% gaming-tax substrate

- Structure: 100% share purchase (licences attach to the entity)

- Headline cost: >€3.5M price + €1M DGOJ guarantee + €250k broker = ~€4.75M cash, plus migration / DD / counsel

- NBO deadline (Fabrice): end May 2026; seller targets close by year-end

- 21-point pre-LOI questions sent 19 May; reply received 22 May

- 5 / 21 substantively answered; 6 CRITICAL deferred post-LOI; Q17–20 "to follow"

- NDA not yet signed — Fabrice wants the NBO first (sequencing risk)

- FY24 audited: Rev €31.1M · Op loss €794k · Net loss €634k

- FY25 unaudited: Rev €34.4M (+10.8%) · Op loss €1.44M · Net loss €1.12M (+77% worse)

- Equity 31/12/25: −€3.83M (Art. 363 dissolution; cure ~€3.91M)

- Intra-group debt: €4.83M (+€2.2M YoY — parent funding losses)

- Off-balance contingent: €182.9M parent guarantees (co-obligor)

- 2 DGOJ licences: €2.4–2.7M (Fabrice comp range)

- ~10k player database: €0.5–1.0M (migration churn)

- Time-to-market vs DGOJ de novo: €0.5–1.0M premium

- Melilla tax substrate: ~€0 net NPV (€280k saving ≈ €275k substance cost)

- Fair value €3.4–4.7M — current ask sits at the top

| Scenario | Net cash | Time | Contingent |

|---|---|---|---|

| S1 · Acquisition with cleansing | €5.1M | 3–6 mo | — |

| S2 · Acquisition without cleansing | €14.9M | 3–6 mo | €182.9M |

| S3 · DGOJ de novo (build) | €4.85M | 12–18 mo | — |

- €182.9M parent guarantees — release letters required from 3 lender groups

- €8.74M cleansing bill if seller refuses intra-group debt + Art. 363 cure

- Melilla regime — no AEAT inspection history confirmed; retroactive tax exposure

- BIN €13M+ tax losses likely forfeited on change of control (~€2.6M shield lost)

- Approve NBO at €2.4–2.7M (not the €3.5M ask), conditional on 5 written pre-LOI deliverables

- Approve budget for independent Spanish gaming + tax counsel (~€180k)

- Authorise request for Grupo Orenes consolidated audited accounts (parent credit)

- Pre-approve walk-away to Scenario 3 if seller refuses any CRITICAL mitigation in writing

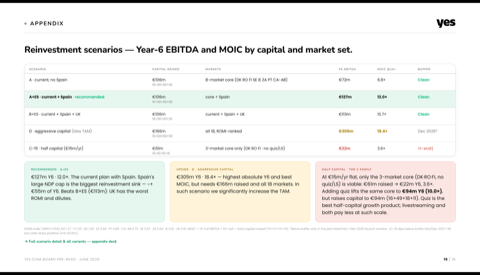

- Spain's large NDP cap is the biggest reinvestment sink — it adds ~€55m of Y6 EBITDA (recommended plan €127m with Spain vs €72m without). Acquisition is the only route into the market.

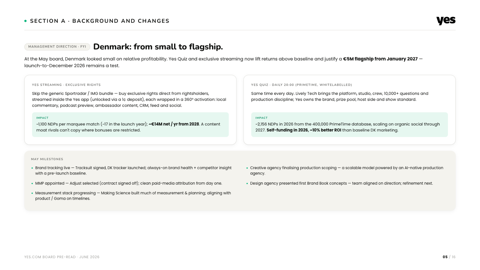

Denmark: from small to flagship.

At the May board, Denmark looked small on relative profitability. Yes Quiz and exclusive streaming now lift returns above baseline and justify a €5M flagship from January 2027 — launch-to-December 2026 remains a test.

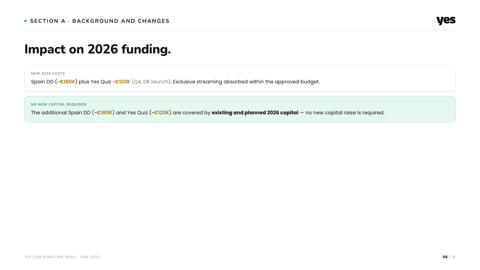

Impact on 2026 funding.

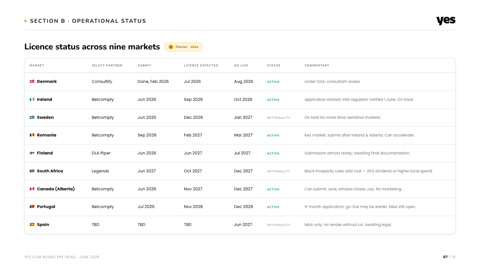

Licence status across nine markets

Financial update.

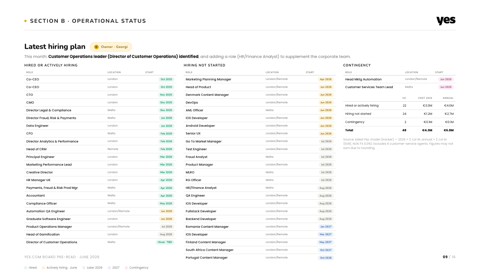

Latest hiring plan

| Role | Location | Start |

|---|---|---|

| Co-CEO | London | Oct 2025 |

| Co-CEO | London | Oct 2025 |

| CTO | London | Nov 2025 |

| CMO | London | Dec 2025 |

| Director Legal & Compliance | Malta | Dec 2025 |

| Director Fraud, Risk & Payments | Malta | Jan 2026 |

| Data Engineer | London | Jan 2026 |

| CFO | Malta | Feb 2026 |

| Director Analytics & Performance | London | Feb 2026 |

| Head of CRM | Remote | Feb 2026 |

| Principal Engineer | London | Mar 2026 |

| Marketing Performance Lead | London | Mar 2026 |

| Creative Director | London | Mar 2026 |

| HR Manager UK | London | Apr 2026 |

| Payments, Fraud & Risk Prod Mgr | Malta | Apr 2026 |

| Accountant | Malta | Apr 2026 |

| Compliance Officer | Malta | May 2026 |

| Automation QA Engineer | London/Remote | Jun 2026 |

| Graduate Software Engineer | London | Jun 2026 |

| Product Operations Manager | London/Remote | Jul 2026 |

| Head of Gamification | London | Aug 2026 |

| Director of Customer Operations | Malta | Hired · TBD |

| Role | Location | Start |

|---|---|---|

| Marketing Planning Manager | London/Remote | Apr 2026 |

| Head of Product | London/Remote | Jun 2026 |

| Denmark Content Manager | London/Remote | Jun 2026 |

| DevOps | London/Remote | Jun 2026 |

| AML Officer | Malta | Jun 2026 |

| iOS Developer | London/Remote | Jun 2026 |

| Android Developer | London/Remote | Jun 2026 |

| Senior UX | London/Remote | Jun 2026 |

| Go To Market Manager | London/Remote | Jul 2026 |

| Test Engineer | London/Remote | Jul 2026 |

| Fraud Analyst | Malta | Jul 2026 |

| Product Manager | London/Remote | Jul 2026 |

| MLRO | Malta | Jul 2026 |

| RG Officer | Malta | Jul 2026 |

| HR/Finance Analyst | Malta | Aug 2026 |

| QA Engineer | London/Remote | Aug 2026 |

| iOS Developer | London/Remote | Aug 2026 |

| Fullstack Developer | London/Remote | Aug 2026 |

| Backend Developer | London/Remote | Aug 2026 |

| Romania Content Manager | London/Remote | Jan 2027 |

| iOS Developer | London/Remote | Mar 2027 |

| Finland Content Manager | London/Remote | May 2027 |

| South Africa Content Manager | London/Remote | Oct 2027 |

| Portugal Content Manager | London/Remote | Oct 2028 |

| Role | Location | Start |

|---|---|---|

| Head Mktg Automation | London/Remote | Jun 2026 |

| Customer Services Team Lead | Malta | Jun 2026 |

| HC | Cost 2026 | Annual | |

|---|---|---|---|

| Hired or actively hiring | 22 | €3.0M | €4.0M |

| Hiring not started | 24 | €1.2M | €2.7M |

| Contingency | 2 | €0.1M | €0.1M |

| Total | 48 | €4.3M | €6.8M |

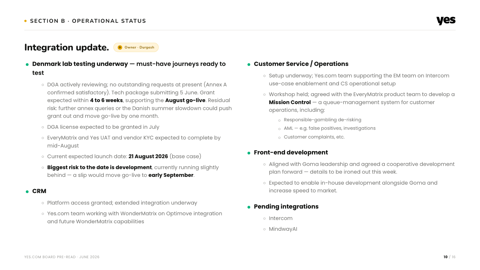

Integration update.

- Denmark lab testing underway — must-have journeys ready to test

- DGA actively reviewing; no outstanding requests at present (Annex A confirmed satisfactory). Tech package submitting 5 June. Grant expected within 4 to 6 weeks, supporting the August go-live. Residual risk: further annex queries or the Danish summer slowdown could push grant out and move go-live by one month.

- DGA license expected to be granted in July

- EveryMatrix and Yes UAT and vendor KYC expected to complete by mid-August

- Current expected launch date: 21 August 2026 (base case)

- Biggest risk to the date is development, currently running slightly behind — a slip would move go-live to early September.

- CRM

- Platform access granted; extended integration underway

- Yes.com team working with WonderMatrix on Optimove integration and future WonderMatrix capabilities

- Customer Service / Operations

- Setup underway; Yes.com team supporting the EM team on Intercom use-case enablement and CS operational setup

- Workshop held; agreed with the EveryMatrix product team to develop a Mission Control — a queue-management system for customer operations, including:

- Responsible-gambling de-risking

- AML — e.g. false positives, investigations

- Customer complaints, etc.

- Front-end development

- Aligned with Goma leadership and agreed a cooperative development plan forward — details to be ironed out this week.

- Expected to enable in-house development alongside Goma and increase speed to market.

- Pending integrations

- Intercom

- MindwayAI

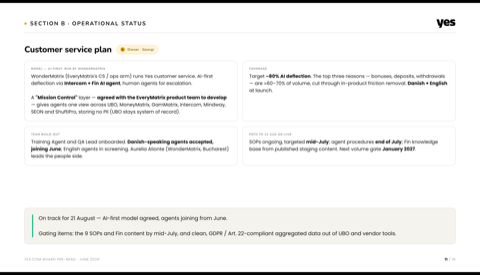

Customer service plan

A "Mission Control" layer — agreed with the EveryMatrix product team to develop — gives agents one view across UBO, MoneyMatrix, GamMatrix, Intercom, Mindway, SEON and ShuftiPro, storing no PII (UBO stays system of record).

Gating items: the 9 SOPs and Fin content by mid-July, and clean, GDPR / Art. 22-compliant aggregated data out of UBO and vendor tools.

Our approach to Product — the social-feed mechanic, applied to iGaming.

We firmly believe in our product operating model, challenging the traditional Product Manager role and approach.

What we need from the board.

Reinvestment scenarios — Year-6 EBITDA and MOIC by capital and market set.

Reflection after the last investor meeting.

Two questions from the last investor meeting deserve a sharper answer:

why do you need the money, and what does it fund.

Under this frame: we do not need new capital to build a profitable business in Denmark and 1 to 2 follow-on markets. We need it if we want to be a €1B+ business in 5 years across 8 to 20 markets.

The capital determines speed and breadth, not viability.

This is a stronger posture. The investor picks their level of ambition.

We are not asking them to fund our survival.

We are asking them to fund the upside trajectory.